|

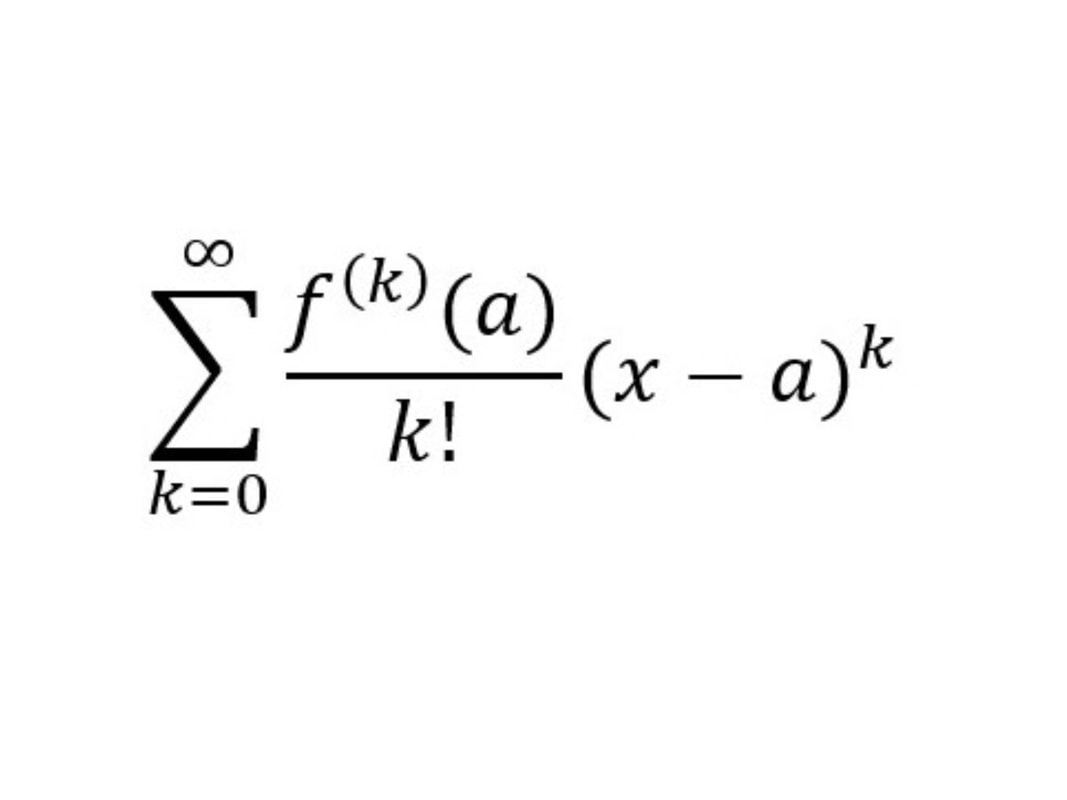

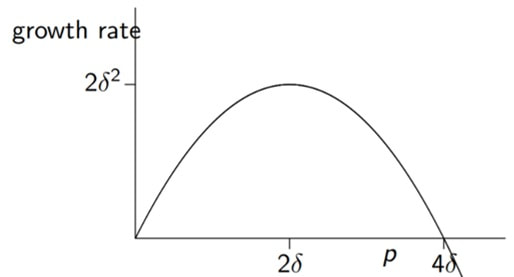

Long Him Lui (guest writer) Investment comes in two forms: trading strategy and money management. Money management refers to how you choose to reinvest the money that you have earned, ignoring the inflow of new funds into your account by entering new positions with the same transactional volume as prior or increasing exposure to assets proportionately to balance risk. The Kelly criterion, also known as the scientific gambling method, is a risk management method which almost guarantees higher wealth in the long run compared to any other strategy. The Kelly criterion states that, theoretically, as you increase the number of bets x to infinity, your wealth will be maximised in the long run compared to any other betting strategy. The way this is done is by maximizing the logarithm of wealth, which is an attempt to increase the geometric ratio, or the growth rate. To simplify, assuming that an investment trading plan is separated into incremental steps, by maximizing the logarithm of wealth, we are trying to maximize the rate of increase per increment while accounting for risk. Proof As stated previously, the Kelly criterion is aimed to maximize the expected value of the logarithm of wealth. The expected value is given by:  Where x denotes a particular outcome, P(x) denotes the probability for that outcome to occur, and n is the total number of outcomes possible. Let us consider one unit of wealth. Taking a fraction f of it that occurs with probability p and offers odds b, the probability of winning will be p and the new amount of wealth after a win will be 1 + fb. The probability of losing will be 1 - p, since this is a two-outcome system where you either win or lose, and the sum of all probabilities in a system must be 1. The amount of wealth after a loss will then be 1 - f. Placing everything in terms of the logarithm of wealth (where we define log W = E), we get:  The form directly above is equivalent to the summation shown further above, where we take the outcome of a victory (1 + fp) and multiply it by the probability of this happening (p), then summing it with the likes of the loss. To find the maximum value of the logarithm of wealth, we can differentiate the above expression with respect to f. To learn about optimisation through differential calculus, check out these videos on Khan Academy.  Here, f* denotes the value of f when the original unit of wealth is maximized. Rearranging to find f*, we get:  This can be further rearranged to:  Here, p represents the probability of a win, 1-p represents the probability of a loss, and b represents the payout. We can write this expression in terms of words:  In terms of investment and trading, the payout can be interpreted as:  Kelly Graph Even though there is an optimal amount of wealth to risk per transaction, there are also many intermediate values that can be invested. We can calculate the best possible value to risk to maximize wealth. Suppose that there is an investment that is considered risky and another that is considered risk-free that pays interest rate r. If we plot this on a graph, we get:  The y-axis of the graph represents the returns or growth rate and the x-axis represents the percentage risked. We can determine visually that the asymptotic growth rate can be modelled as a quadratic of p. To maximise growth rate, the Kelly Criterion suggests taking p = 2δ, which should lead to a long-term growth rate of 2δ^2. Any proportion of wealth on the left of the narrow band surrounding 2δ is considered an underinvestment for the long-term. There will still be a positive rate of growth, but will be a suboptimal rate of growth that does not use all economic resources efficiently. Any proportion of wealth on the right of the narrow band surrounding 2δ is considered an over-aggressive investment for the long-term. There is still a positive rate of growth, but will also be suboptimal. Any proportion of wealth that exceeds 4δ is considered a bad investment, since there will most likely be a negative growth rate in the long term. There exists a concept of a half-Kelly. This is the value of δ that is half of the optimized value of 2δ. Investors use the half-Kelly as a more conservative way to achieve growth in returns, since it uses up a smaller proportion of one’s wealth while only sacrificing 25% of the maximized returns. This is can be explained by the parabolic shape of the graph.

0 Comments

|